People are more aware of the benefits of having a well-structured insurance plan. If you have a plan or intend to get one then you also have an idea of the different health insurance coverages available to you. One thing you may not know is what happens in instances when your injury was caused by someone else. This process is called Subrogation.

So, what is subrogation in health insurance? This is a concept that your insurer may use to reimburse their expenses. It’s important to know how this works as it will affect other things like your premiums, court settlements, and out-of-pockets, or help you understand what it means to receive a “subrogation rights” letter.

What Is Subrogation In Health Insurance?

Subrogation in health insurance is the legal right of your insurers to seek payment for damages from a party at fault for your injury. They step into your shoes after already paying for your medical bills.

So, a very common example is usually in the case of being hit by a distracted driver. Your insurance company covers the bills for your injury and afterward seeks reimbursement from the driver’s auto insurance company for those medical costs.

We have helped several customers secure insurance plans that have subrogation clauses included. This system applies to all health insurance, be it individual, family, or group.

Why Subrogation Matters To You

The question on your mind will probably be, “What does this have to do with me?” Subrogation affects you in several ways, directly and indirectly. Most importantly, it lets you know your limits and things you can do. Here are some things it does:

- It prevents double payment: Subrogation prevents you from unjustly receiving payment twice for the same medical bills (i.e. from health insurance and the at-fault party).

- It promotes low premiums: A more beneficial effect is that health insurers who carry out subrogation can maintain more affordable rates because they recover some of their costs back.

- It clarifies financial responsibility – The process ensures that the party who caused your injury ultimately pays for the damages.

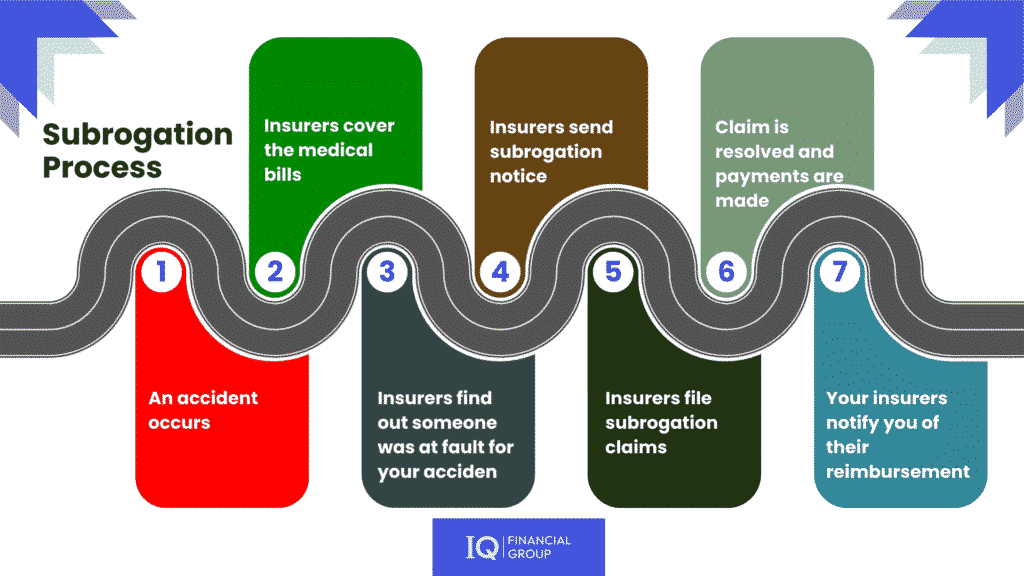

The Subrogation Process Explained

The subrogation process follows a predictable path in most cases:

Step 1: You Get Treatment

After an injury, you seek medical care. This is still the most important part as you have to receive the necessary medical attention before anything can kick in. Your health insurance covers these expenses according to your policy terms. This might include visits to specialists or chiropractors, depending on what health insurance covers in your plan.

Step 2: Your Insurer Investigates

Your insurers review the accident report and evaluate if there are other parties at fault. After this, they decide if pursuing subrogation makes sense.

Step 3: Notice Gets Sent

After careful investigation and decision-making, your insurers notify the responsible party(or their insurance company) about their intention to recover costs.

Step 4: Filing the Subrogation Claim

Your health insurer submits a subrogation claim to the at-fault party’s insurance company. This claim details all the medical expenses they covered for your injuries.

Step 5: Reaching Resolution

The claim gets resolved through one of the following means:

- Direct payment from the at-fault party’s insurer to your health insurance company

- Negotiated settlement between the insurance companies

- Sometimes, a lawsuit if they can’t reach an agreement

Real-World Simulation of Subrogation In Health Insurance

Let’s take a comprehensive look at how the subrogation will work in a real-life situation:

So, Jerry visits his local hardware store and slips on a puddle of water with no warning sign. He breaks his leg and needs surgery costing $40,000. His health insurance company, Ever Guard, covers the rest of his medical bills after he pays his $2,000 deductible.

Ever Guard discovers that the store was at fault for not including the proper cautions. They pursue a subrogation claim against the store’s liability insurance. The store’s insurer agrees to reimburse Ever Guard for the $38,000 they paid for Mark’s treatment.

In this case, subrogation made sure the store’s insurance – not Mark’s health insurance – ultimately paid for the injury their negligence caused.

When Subrogation Typically Happens

Health insurance subrogation most commonly occurs after:

- Car accidents where another driver caused the crash

- Falls on commercial property due to unsafe conditions

- Injuries from defective products that manufacturers should be liable for

- Medical errors resulting in additional treatment needs

Your Rights During The Subrogation Process

You have important rights during subrogation that you should know about:

Getting Fully Compensated First

Many states follow the “made whole doctrine,” which requires you to be fully compensated for your injuries before your health insurer can collect through subrogation. This means your out-of-pocket expenses, pain and suffering, and other damages should be paid first.

Reduced Subrogation Amounts

Your health insurer might lower their subrogation claim if you:

- Paid attorney fees to pursue your claim

- Received a reduced settlement due to insurance limits

- Were found partially at fault for the accident

Information Access

You have the right to know about your health insurance company’s subrogation efforts and how they might impact your claim against the responsible party.

How Subrogation Changes Your Settlement Amount

When you receive a settlement from an at-fault party, your health insurer’s subrogation rights affect how much you keep. They are entitled to the amount they paid in your medical bills so far as it is stated in their policy terms. However, several factors can change this amount, including:

- The specific laws in your state regarding subrogation

- The exact wording in your health insurance policy

- Whether your settlement truly compensated you fully

- Legal fees you paid to get the settlement

Finding Subrogation Terms In Your Policy

Your health insurance policy contains specific language about subrogation rights. Our customers are always directly informed about this by our expert insurance brokers. However, if you are doing your own research, look for sections called “Subrogation Rights,” “Right of Recovery,” or “Third-Party Liability.”

These sections outline your responsibilities, which usually include:

- Telling your health insurer about potential third-party claims

- Not settling claims without getting your health insurer’s approval first

- Helping your health insurer with their subrogation efforts

How Different Health Plans Handle Subrogation

Each type of health insurance approaches subrogation differently:

Private Insurance Companies

Private insurers typically have dedicated subrogation departments and actively pursue recovery. Their policies often contain detailed subrogation language that they enforce strictly.

Government Programs

Medicare and Medicaid have strong subrogation rights backed by federal law. They must pursue recovery of payments when a third party is responsible.

Employer Self-Funded Plans

Self-funded plans governed by ERISA (Employee Retirement Income Security Act) often have the strongest subrogation rights, sometimes overriding state laws that might limit subrogation.

Tips For Dealing With Subrogation

When subrogation becomes part of your insurance claim, follow these recommendations:

- Tell all your insurers quickly about your accident and any potential third-party liability

- Read your policy’s subrogation section to understand your obligations

- Keep records of all communications with insurance companies

- Talk to an attorney if the subrogation claim seems excessive

- Try to negotiate the amount if possible, especially if your settlement didn’t fully cover your losses

When To Get Professional Help

Your insurers can always help fight the good fight for you, all you need to do is to involve them as much as possible. Consider seeking expert guidance about subrogation when:

- You’re dealing with a serious injury claim

- Multiple insurance companies are involved

- Your health insurer wants a large portion of your settlement

- You believe your settlement didn’t fully compensate you

The team at IQ Financial Group can help you navigate these complex situations. Their experience with both disability insurance and health insurance matters gives them unique insight into protecting your financial interests.

The Bottom Line On Health Insurance Subrogation

Subrogation in health insurance plays a vital role in the insurance system. It ensures that costs land with responsible parties, helps maintain reasonable premiums, and supports the financial stability of the insurance market.

As a policyholder, knowing about subrogation helps you:

- Prepare for the process during insurance settlements

- Secure fair compensation for your injuries

- Understand the relationships between your different insurance policies

- Make smarter choices when buying insurance coverage

Take The Next Step With Your Insurance Protection

Our insurance brokers are available to provide you with several types of insurance plans, and while at it they will let you know about the subrogation clauses involved. They can further help you understand how subrogation and other insurance concepts affect your coverage.Contact us today to book a scheduled call about your health insurance needs. We offer a free, no-obligation first-timers free quote. Our team will make sure you have the right coverage to protect yourself and your family, no matter what challenges life brings.